With online financial technology companies ramping up pressure to get into community banking, only the time-tested, traditional community banking model ensures these advancements are not at the expense of customers trust, financial resources, and community wealth.

Just recently, a company named Robinhood Financial LLC advertised a 3% deposit account, and in that advertisement for the account stated that funds would be insured by the Securities Investor Protection Corp (SIPC). Shortly after, the SIPC CEO disagreed that funds in those advertised accounts would be protected by the SIPC, theoretically, leaving customers of Robinhood Financial LLC at risk. (link: https://www.americanbanker.com/articles/robinhood-backs-down-after-outcry-over-checking-account)

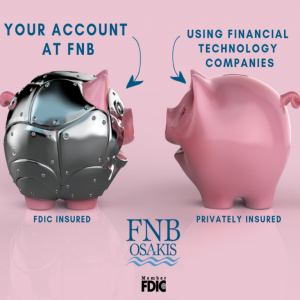

This is just the most notable, and recent, of a rash of Silicon Valley-based financial technology companies that have entered banking market. Many partner with banks to allow their technology to be used in combination with the traditional protections that our Banking industry provide their customers, Federal Deposit Insurance and continual regulatory examinations to ensure the safety and soundness of the place you keep your money.

The most troubling aspect of these financial technology companies trying to separate themselves from the traditional banking industry is the perception that they are as safe as a bank. They are not. Whether you are using PayPal, Venmo, or the most recent, convenient technology, consumers need to be aware that those organizations may have products that operate like a bank, but they do not have the backing of the Federal Deposit Insurance Corporation or the regulatory supervision of the Federal Reserve, FDIC, State, or Office of the Comptroller of the Currency. Balances kept with these companies are not necessarily safe, nor is what the company is doing with the funds you entrust with their institutions.

Independent and locally-owned Community Banks, like the First National Bank of Osakis, are the most logical place to keep your hard-earned dollars the safest, because they are time-tested and consistently regulated. Through the 115 years FNB Osakis has been in existence, it has seen numerous economic cycles, and is focused on the constant risks to our customer’s and community’s financial health.

The best alternative to enjoying convenience without sacrificing risk –open a checking account and make that the only checking account you link to transfer balances between these Financial Technology Companies applications/websites. Keep your other checking account hidden from electronic connections and only transfer the funds in between the two checking accounts. Our Customer Service Concierge can assist you in structuring accounts in this manner, as well as guide you to using your accounts safely in conjunction with Paypal, Venmo, etc.

Over the past 2 years, FNB Osakis has made significant investments in digital ways to use your accounts, backed by the common-sense understanding we have of our customers. We are constantly upgrading and adding features to our Online and Mobile Banking environments to be as safe, and convenient, as possible.

Want to know how much FDIC coverage you have at FNB? Check out this tutorial on FDIC’s EDIE The Estimator. It’s a great resource for our customers to calculate their FDIC coverage, so give it a try!

EDIE the Estimator Link → https://www5.fdic.gov/edie/

What is the FDIC?

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United State government that protects the funds depositors place in banks and savings associations. FDIC insurance is backed by the full faith and credit of the United States Government. Since the FDIC was established in 1933, no depositor has lost a penny of FDIC-insured funds. FDIC Insurance covers all deposit accounts including:

- Checking Accounts

- Savings Accounts

- Money Market Deposit Accounts

- Certificates of Deposit

FDIC Insurance does not cover other financial products and services that banks may offer, such as stock, bonds, mutual funds, life insurance policies, annuities or securities.

The standard insurance amount is $250,000 per depositor, per insured bank, for each ownership category.

More Information on Regulation E

The Consumer Financial Protection Bureau’s Regulation E (“Regulation E”) provides a basic framework that establishes the rights, liabilities and responsibilities of participants in “electronic fund transfer” systems. This framework provides consumers with certain protections for personal deposit accounts. A “consumer” means a natural person and, therefore, Regulation E protections apply to consumer accounts established primarily for personal, family or household purposes.

The term “electronic fund transfer” (EFT) generally refers to a transaction initiated through an electronic terminal, telephone, computer or magnetic tape that instructs a financial institution either to credit or debit a consumer’s deposit account. Examples of electronic fund transfers include automated teller machine (ATM) transactions, point-of-sale (POS) or purchase transactions done using a debit card and pre-authorized transfers from or to an account (such as direct deposits).

Links to more information:

FAQ from the FDIC: https://www.fdic.gov/deposit/deposits/faq.html

Overview from the FDIC: https://www.fdic.gov/deposit/deposits/

Insured or not insured: https://www.fdic.gov/consumers/consumer/information/fdiciorn.html

Regulation E, demands bank insures against fraud: https://www.federalreserve.gov/boarddocs/supmanual/cch/efta.pdf

Bank Customer’s guide to Cyber Crime: https://www.fdic.gov/consumers/consumer/news/cnwin16/FINAL_Color_CN_Winter2016.pdf

How FDIC Insurance Works: https://www.thebalance.com/fdic-insurance-315761